5.9% CAGR Revealed: How MAP Technology and Sustainability are Pushing Seafood Packaging to $15.8B

Seafood Packaging Market Poised to Reach US$ 15.83 Billion by 2029, Propelled by a 5.9% CAGR: Unveiling Sustainable Innovations, Regional Dominance, and Strategic Future Decisions

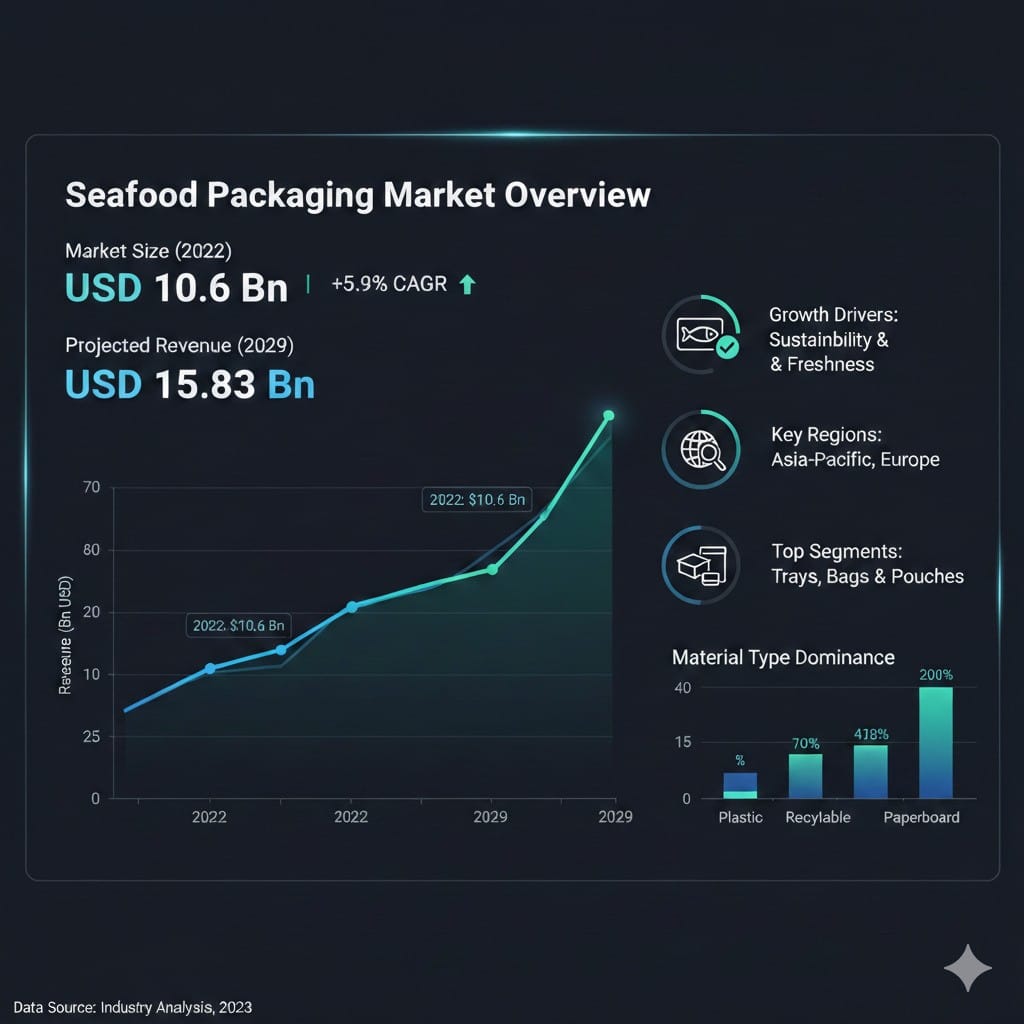

Maximize Market Research, a preeminent global market intelligence and corporate consulting firm, has formally released its most recent, meticulously researched comprehensive report titled, "Global Seafood Packaging Market: Industry Analysis and Forecast (2023-2029)." According to the extensive data and analytical forecasting presented in this publication, the global seafood packaging market, which held a valuation of US$ 10.06 Billion in the base year of 2022, is anticipated to embark on a steady upward trajectory. The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.9% over the forecast period, culminating in an estimated market size of US$ 15.83 Billion by the end of 2029.

This sweeping report provides an all-encompassing view of the shifting paradigms within the seafood and marine products supply chain, specifically examining how packaging methodologies are evolving to meet stringent regulatory standards, prolonged shelf-life requirements, and the eco-conscious demands of the modern consumer. Furthermore, the publication serves as an invaluable blueprint for investors, packaging manufacturers, food processing entities, and policymakers by highlighting the "future decisions" required to navigate this dynamic commercial landscape successfully.

Get the Edge: Download Your Exclusive Strategy Guide & PDF Brochure Today @ https://www.maximizemarketresearch.com/request-sample/54412/

The Evolving Landscape of Seafood Consumption and Packaging Integration

Seafood—encompassing a diverse array of fish, crustaceans, mollusks, and other aquatic life—has long been a cornerstone of global diets. However, in recent years, there has been a massive paradigm shift in consumer eating habits. As global populations become increasingly health-conscious, there is a pronounced pivot away from heavy red meats toward the lean protein, high vitamins, zinc, calcium, and vital long-chain omega-3 fatty acids abundantly found in marine products.

Despite its nutritional superiority, seafood presents a unique logistical challenge: it is highly perishable. Compared to terrestrial meats, fish and shellfish lose their freshness and succumb to spoilage at an exponentially faster rate. The primary objective of seafood packaging is, therefore, to provide an impenetrable barrier against dehydration, lipid oxidation, and microbial contamination. The Maximize Market Research report underscores that the surging global appetite for fresh, ready-to-cook, and healthy marine products is the primary engine driving the demand for advanced, highly reliable packaging solutions.

As consumers increasingly demand transparency, quality, and convenience, the packaging sector is being forced to adapt. The modern shopper expects seafood to look freshly caught, even if it has traversed oceans to reach the supermarket shelf. Consequently, the packaging is no longer just a protective vessel; it is a critical instrument of preservation, quality assurance, and brand communication.

Technological Innovations: The Shift Towards Sustainable and Smart Packaging

The global push toward environmental sustainability is dramatically reshaping the seafood packaging sector. For decades, the industry relied heavily on conventional plastics that contributed significantly to environmental degradation. Today, the narrative has changed. The report highlights a massive influx of innovation directed at minimizing the carbon footprint of marine packaging.

Industry heavyweights are actively redefining material sciences. For instance, in July 2020, Amcor plc introduced SkinNova, a revolutionary seafood packaging solution that slashes plastic usage by an impressive 70% compared to traditional Modified Atmosphere Packaging (MAP). This innovation not only drastically reduces plastic waste but also cuts the associated carbon footprint by 45%. Similarly, Sealed Air Corporation has made monumental strides by launching versions of its iconic packaging materials formulated with up to 90% recycled content, alongside strategic acquisitions aimed at bolstering high-reliability, automated, and eco-friendly bagging systems.

Beyond sustainability, technological functionality is advancing rapidly. The report identifies that intelligent packaging—incorporating time-temperature indicators, freshness sensors, and leakage detectors—is transitioning from a niche concept to a mainstream necessity. Active food packaging, which utilizes oxygen scavengers and moisture regulators, is also gaining massive traction, ensuring that the biochemical integrity of the seafood is maintained from the processing plant to the consumer's kitchen.

Overcoming Industry Hurdles: The Threat of Marine Pollution

While the market exhibits robust growth potential, the Maximize Market Research report does not shy away from detailing the severe macroeconomic and environmental restraints hindering the industry. The most pressing of these challenges is the escalating level of global water pollution.

Industrial effluents, agricultural pesticide runoff, crude oil spills, and municipal waste are continually degrading marine habitats. This influx of toxic compounds leads to severe acute and chronic impacts on fish populations—ranging from suppressed immune systems and delayed metabolism to physical ailments like gill illness and tissue ulceration. Ultimately, these ecological disasters lead to a direct decline in the harvestable yield of quality seafood. A contraction in the primary seafood market invariably cascades down the supply chain, directly inhibiting the growth potential of the seafood packaging industry. Market players must recognize that their commercial viability is inextricably linked to the ecological health of the world's oceans.

Deep Dive into Market Segmentation

To provide a granular understanding of the market dynamics, the report segments the global seafood packaging industry by Material, Product, Technology, and Seafood Type.

By Material: The Persistent Dominance of Plastic

Despite the overarching push for eco-friendly alternatives, the plastics segment currently dominates the global market and is projected to retain the highest revenue share throughout the 2023-2029 forecast period. The inherent properties of plastic—including superior water resistance, impermeability to moisture, resistance to airborne pollutants, and overall cost-effectiveness—make it incredibly difficult to replace. Plastic completely mitigates the risks of oxidation and chemical interference, ensuring maximum food safety. The future, however, lies in the evolution of this segment toward advanced bioplastics and highly recyclable polymer blends that offer the functional benefits of traditional plastics without the associated environmental toll.

By Technology: Modified Atmosphere Packaging (MAP) Leads the Way

In the realm of packaging technology, the Modified Atmosphere Packaging (MAP) segment asserts undeniable dominance. MAP involves deliberately altering the gaseous environment surrounding the seafood product within the package. By introducing a carefully calibrated mixture of nitrogen and carbon dioxide—which acts as an antimicrobial agent—MAP effectively stalls lipid oxidation and inhibits aerobic bacterial proliferation. This technology dramatically extends the shelf life of fresh fish and shellfish without the need for artificial chemical preservatives, perfectly aligning with consumer demands for natural, unprocessed foods. Vacuum packaging and vacuum skin packaging are also highlighted as rapidly growing sub-segments, particularly for premium and frozen seafood offerings.

By Product and Seafood Type

The market is further categorized by product formats, including trays, bags and pouches, food cans, boxes, and shrink films. Trays and pouches are witnessing accelerated demand due to their convenience and compatibility with MAP and vacuum skin technologies. Regarding seafood types, the market caters to fish, mollusks, crustaceans, and others. The packaging requirements vary wildly across these types; for example, the rigid, puncture-resistant packaging required for crustaceans differs vastly from the flexible, transparent films utilized for filleted fish.

Regional Blueprint: Asia-Pacific Takes the Helm

From a geographic standpoint, the Asia-Pacific (APAC) region stands as the undisputed titan of the global seafood packaging market. The region's dominance is multifaceted. Firstly, Asia is geographically surrounded by expansive coastlines, making seafood a primary, daily dietary staple for billions of people. Countries like China, Japan, South Korea, and emerging Southeast Asian nations are among the highest consumers of marine products globally.

Furthermore, the APAC region is witnessing a massive surge in commercial aquaculture and seafood processing. The easy availability of raw packaging materials from the southern and eastern industrial corridors of Asia significantly lowers production costs. Coupled with rising disposable incomes, rapid urbanization, and an increasing middle-class awareness regarding the consumption of hygienically packed, fresh seafood, the Asia-Pacific market represents the most lucrative battleground for global packaging manufacturers.

North America and Europe also maintain highly significant market shares. These regions are characterized by stringent food safety regulations set forth by bodies like the FDA and EFSA, which necessitate the use of premium, high-barrier packaging solutions. Additionally, consumers in these Western markets exhibit a high willingness to pay a premium for sustainably sourced and eco-friendly packaged seafood, driving innovation in biodegradable and recyclable material segments.

Competitive Frontier: Strategies of Market Leaders

The competitive landscape of the global seafood packaging market is fiercely contested, populated by a mix of entrenched multinational corporations and agile, innovative emerging players. The Maximize Market Research report profiles key industry titans, including Sealed Air, Amcor plc, DS Smith, Bemis (Amcor), Pactiv (Reynolds), Berry Global, Constantia Flexibles (Wendel), Winpak, Coveris, Clondalkin Group, Cascades, DOW, Smurfit Kappa, and ULMA Packaging, among others.

These market leaders are currently engaged in intense strategic maneuvering. The dominant growth strategies include massive investments in Research and Development (R&D) to pioneer proprietary, lightweight, and sustainable materials. Mergers and acquisitions (M&A) are also prevalent, as larger entities absorb niche manufacturers of automated packaging machinery or specialized sustainable materials to rapidly expand their technological portfolios. For instance, ULMA Packaging's recent initiatives to develop innovative packaging machines designed to minimize packaging size, reduce waste, and seamlessly process biodegradable films highlight the industry's shift toward operational efficiency intertwined with environmental stewardship.

Future Decisions: Strategic Imperatives for Stakeholders

The data and trends meticulously compiled in this report highlight several critical "future decisions" that businesses, investors, and policymakers must make to thrive in the impending commercial landscape.

1. Strategic Transition to Circular Economy Models: The foremost future decision for packaging manufacturers is the definitive pivot toward a circular economy. The reliance on single-use, non-recyclable plastics is rapidly becoming a commercial liability due to evolving global legislations and shifting consumer loyalties. Executives must decide now to aggressively reallocate capital toward the development of biodegradable polymers, mono-material structures that are easily recyclable, and packaging designs that utilize high percentages of post-consumer recycled (PCR) content.

2. Integration of Smart Supply Chain Technologies: Investors and corporate leaders must make the strategic decision to integrate Internet of Things (IoT) technologies into packaging solutions. The future of seafood packaging lies in traceability. Incorporating QR codes, RFID tags, and biochemical freshness indicators will allow consumers and retailers to track the exact origin, cold-chain history, and current quality status of the seafood. Companies that decide to lead in "smart packaging" will capture premium market segments.

3. Geopolitical and Supply Chain Diversification: Given the disruptions witnessed in global trade, supply chain managers must make future decisions regarding the localization of their packaging material sourcing. Relying entirely on overseas suppliers for vital packaging components poses a severe risk to operational continuity. Companies must decide to diversify their supplier base and build localized manufacturing hubs, particularly in high-growth regions like Southeast Asia and the Middle East, to ensure resilience against global shocks.

4. Collaborative Environmental Stewardship: Seafood packaging companies can no longer view marine pollution as an external issue; it is a direct threat to their foundational supply chain. Future corporate decisions must involve active participation in, and funding of, marine conservation initiatives. By partnering with global NGOs to clean oceans and promote sustainable fishing practices, packaging companies can secure their long-term raw material (seafood) pipeline while simultaneously building immense brand equity and consumer trust.

5. Capitalizing on E-commerce Logistics: The exponential rise of online grocery shopping and direct-to-consumer (D2C) seafood delivery services requires distinct packaging formats. Decision-makers must invest in developing ultra-durable, thermal-regulating, and leak-proof packaging solutions specifically optimized for the rigors of e-commerce transit. The companies that decide to tailor their product lines to the e-commerce boom will secure a dominant competitive advantage over those catering solely to traditional brick-and-mortar retail.

Conclusion

The Global Seafood Packaging Market is standing at a critical evolutionary juncture. The forecast period leading up to 2029 will be defined by the delicate balancing act between maintaining maximum food safety and achieving aggressive environmental sustainability goals. As the market swells toward the US$ 15.83 Billion mark, the victors will be those organizations that proactively embrace material innovation, leverage smart technologies, and make the bold future decisions necessary to align commercial objectives with global ecological health. Maximize Market Research’s latest report serves as the definitive guide for navigating this complex, lucrative, and rapidly transforming global industry.

For a deeper dive into the data, comprehensive segment breakdowns, and to purchase the full report, please visit the Maximize Market Research website: https://www.maximizemarketresearch.com/market-report/global-seafood-packaging-market/54412/

About Maximize Market Research: Maximize Market Research is a multifaceted market research and consulting company encompassing professionals from various industries. We cover sectors including medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To provide clients with a clear vision of their future, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.